Who is fixing the finance gap?

How data & technology are ushering a new era of business financing, from the lessons of M-Kopa to the success of Untapped Global

The Internet promised us a dematerialized society, where information, services, and money would travel through its digital rails at the speed of light.

Software - with almost zero cost of replication and distribution - would be the new oil.

The world would be a global village where prosperity & democracy would triumph.

LMAO 😅

There is some truth to this early 2000s tecno-optimism.

I am writing this article from my bedroom. Thanks to Linkedin, Substack, Gmail, I can distribute my content for free and be part of global conversations.

If I push hard on data analytics, I can learn how to better engage with my audience and eventually upsell a paid subscription (at best), or cross-sell healthy ginger drinks and productivity courses (at worst).

How many gatekeepers have I avoided thanks to a bunch of geeks wearing pajamas, writing code in their dorms, and playing Dungeons & Dragons?

And even if we zoom out and think about the continent, we can say the Internet Revolution has partly delivered on its promise. How many Africans have benefited from access to financial services, remote job opportunities, better & tailored education, and free entertainment? A whole lot!

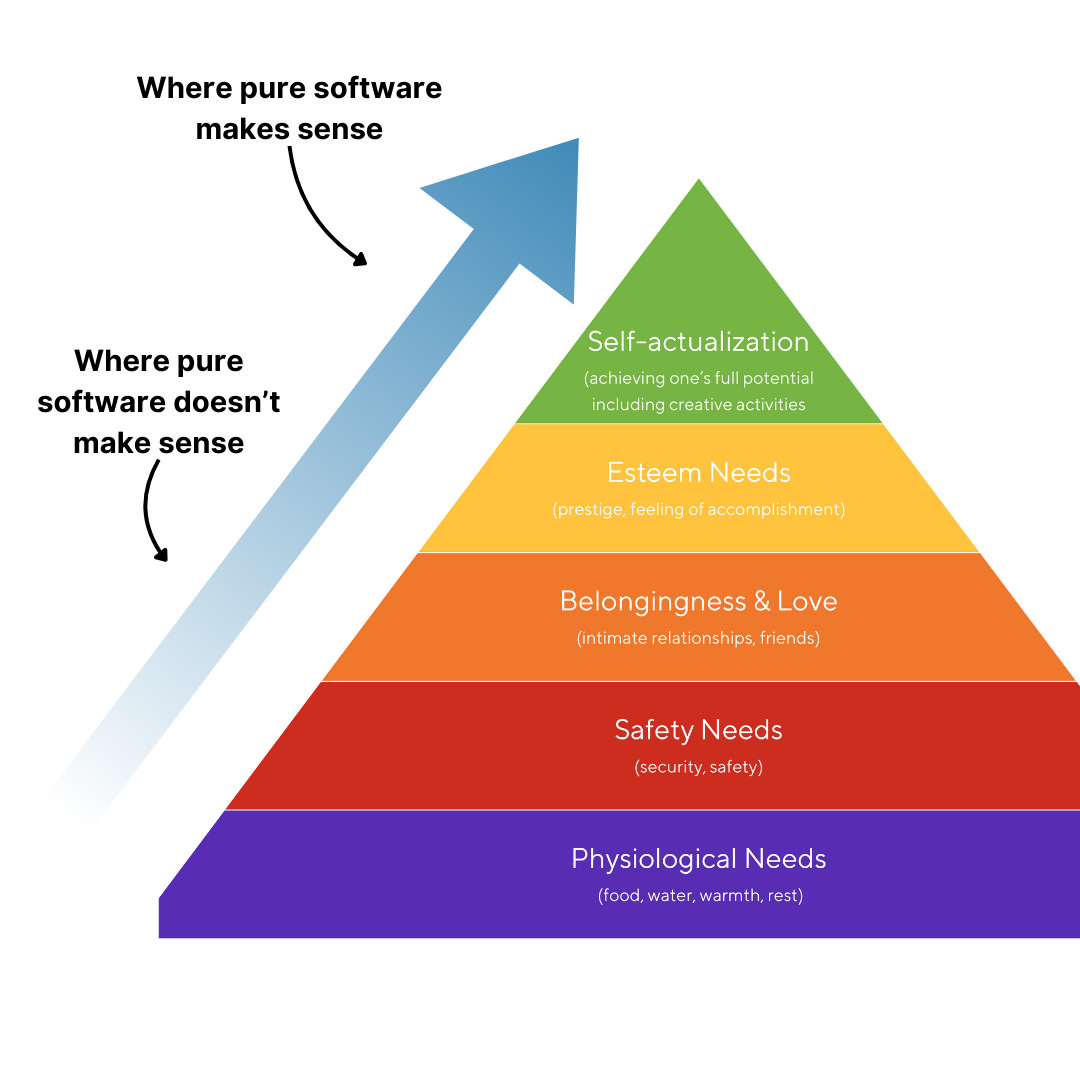

There is a problem with this story, though. The problem with the Digital Eden narrative is that it omits one crucial, underlying assumption: software is only useful when it sits “on top” of something.

We don’t eat software, we don’t shelter with software, we don’t commute with software, we don’t irrigate our lands with software.

Software enables, software improves. Software does not make.

To say it with the Maslow Pyramid: pure software is useful at the top, not at the bottom.

You can leapfrog landline internet because everyone has a mobile phone, fine.

But you can’t leapfrog the two fundamental layers on top of which software can unlock its benefits: physical assets and business structures, to move atoms & transform raw stuff.

Digital technology comes as a booster/equalizer. We might not eat software, but we can improve the productivity of agricultural land with software. Sure, once we have functioning water pipes and businesses taking care of them.

In short, as much as we’d love to live in the metaverse, the economy needs physical, productive assets to deliver your food to the table, your 🍑 to the office, and even your email to the server. And it needs business structures that organize these assets, maintain them, and invest in them, from microscopes to trucks to refrigerators.

And…. here we come to the ❤️ of this article:

In Africa, most of these “business structures” are small-sized, informal businesses.

They desperately need financing to buy, upgrade, and maintain these physical assets.

They can’t get it (SMEs’ finance gap accounts for $136 billion 🥲)

So let me raise the following question then: if software cannot replace tractors & sewing machines, can it at least make us better at funding them? Can technology help us respond to African businesses’ capital needs?

Big Problems 🗻 x Old Incumbents 👴🏽 =New Opportunities 🦋

When we think of financing, we instinctively think of banks.

In Africa, they don’t always have a good reputation.

To cite Kwamena Afful, co-founder of Microtraction in an episode of The Flip:

“African banks mobilize deposits from big enterprises, governments, and high net worth individuals, and deploy these deposits in treasury bills and federal debt. That’s their business model. They are not interested in lending to consumers or small businesses”.

It’s a punchline, but there is some truth to it.

Private credit levels are pretty low in Africa, and when it comes to SMEs, things get even dryer. As the infamous report from Proparco highlights, banks’ loans devoted to small firms in Africa “represent half of that of their counterparts in developing economies” (5% vs 13%). On top of that, only 68.7 % of SMEs loan applications are approved by banks in Africa, against 81.4 % in other developing countries.

But wait: SMEs in the continent account for 40% of GDP and 80% of employment.

So what are banks even doing with their time? Why don’t they just go out there and finance these businesses?

Of course, the answer is “complex”. But apart from banks’ problems with upstream access to capital (read: global investor shying away and crazy high interest rates), I think the main reason is:

ineffective due diligence: the methodology used to assess the credit risk of the borrower

lack of data: the data input needed for the risk management models to work

Let me clarify.

You generally have 3 macro-categories of lending practice:

collateral-based lending

cash flow-based lending

relationship-based lending

Collateral-based lending relies on tangible assets, such as real estate or equipment, that the borrower pledges as security for the loan.

This is an obstacle for many SMEs in the continent as:

they lack eligible assets to pledge as collateral;

the value of collateral assets can be required to be up to 80-100% of the value of the loan (IFC);

movable assets - like inventory and receivables - are not accepted as collateral;

assets’ appraisal is complex and can lead to operational overhead and increased risk

This makes collateral-based lending complex, expensive, and often unfeasible.

Cash flow-based lending focuses on the borrower’s ability to generate sufficient cash flow from operations to meet debt obligations.

To do that, you usually need two things:

income statements & balance sheets: to assess the future cash flows of the borrower

market data & market intelligence: to assess the health of the sector the company operates in

Guess what? Both things are very hard to find in the context of African SMEs.

Many SMEs barely maintain the financial records needed for income statements.

And and if you’ve ever tried to do some market research on the region you know that market intelligence is non-parvenu.

So what?

Lack of collaterals and hard-to-predict cash-flows makes these businesses 1) riskier according to banks’ current credit risk models, and 2) costly, in terms of due diligence costs, which are not justified by the size of the loan.

This is why, ultimately, African banks prefer to finance large enterprises (who usually don’t face these problems) and resort to relationship-based lending practices, which stress the borrower’s history, character, and overall trustworthiness developed through previous interactions.

#saaaad 😢

If we could find a way to lighten lending operations, access data more easily, and upgrade risk-management models, would we be able to finance more physical assets?

Is there a way technology can help us overcome these challenges?

Welcome to the world of “smart” assets… 🧠🛠️

During the past decade, several companies have come up with unique approaches to solve the finance drought of the “unbanked.

An interesting case, making the headlines for its innovative approach to financing, is Kenya’s gemstone: M-Kopa.

They have pioneered a new way to finance high-value consumer goods such as off-grid solar systems, smartphones, TVs, and refrigerators.

How did M-Kopa solve for lowering operations costs and improving data availability? With the clever combination of 3 technologies: mobile money, IoT (SIM cards) embedded in their products, and remote locking technologies.

If I borrow a smartphone with M-Kopa:

the loan is secured by the asset provided, i.e. the smartphone;

I pay daily installments with mobile money;

If I fail to pay, a remote trigger will lock my phone, so that I won’t be able to use it anymore (except for charging money to pay the amount due 😅)

The same holds for a solar system and any other product. Transparent data on assets’ usage and repayments, coupled with remote control over the asset, has proved an effective instrument in establishing initial trust with borrowers.

My repayment rates are then used for credit scoring, enabling me to access further cash loans once the smartphone is paid in full, with the phone resecured as collateral (again).

As simple as it seems, this model alone unleashed a lot of money and a lot of impact. As the GSMA report says:

“The explosive rise of pay-as-you-go (PAYG) in the off-grid energy sector, for example, has played a significant role in widening access to energy. Combining mobile money systems with machine-to-machine (M2M) communication and remote locking has made off-grid energy products more accessible and affordable to billions worldwide, bringing power for the first time to 25-30 million people worldwide between 2015 and 2020”

The recipe for success: a mix of operational excellence, IoT technology and digital payments.

Great!

While this model proved valuable for consumers, we must remember that we want to finance businesses!

M-Kopa lends essentials with a relatively low price tag.

Is there a way we can draw from the lessons of this model and apply them to finance physical, productive assets that cost more money?

…& the world of Untapped’s smart financing 🧠✨

Back in 2021, I tried to put money into an investing vehicle by the name of Untapped Global.

I was intrigued by their model as it combined all the ingredients I was looking for at the time: a data-driven approach; a high-returns portfolio; and a tangible, positive social impact.

It turned out that I wasn’t an accredited investor and I couldn’t invest with them (sigh 😞), so I eventually ended up switching to Daba (who I didn’t know yet at the time).

However, I’ve kept an eye on them over the years, until I could finally sit down with Lundie Strom, Untapped’s Investor Relations & Partnerships Head, to chat and get a better overview of their model.

The fascinating conversation that followed convinced me that they may be on the right track: taking the best of M-Kopa and adding their own twist to it.

I’ll go through what I consider to be the four pillars of their model:

Revenue-share

Operating partners

Iterative approach

Real-time data

Bear with me friends ❤️

1) Revenue-based financing 💸💸💸

One of Africa’s most-funded startups, Moove, recently made the headlines as it received a 100M investment from Uber, valuing the company at 750M.

Its main business model? Revenue-based vehicle financing.

In a revenue-based financing (or revenue-share) agreement, a business receives funding in exchange for a percentage of its future revenue until a specified amount is repaid.

Instead of a fixed amount of money (+ interest rate) to be paid at regular intervals, as with traditional loans, revenue-share repayments fluctuate with the business’s income, providing flexibility during low-revenue periods and faster repayment times during bonanza: investors’ returns are aligned with the company’s performance.

In the case of Moove, they finance cars for Uber drivers. The loan is repaid with a share of the revenues the Uber driver makes: as simple as that.

At a high level, Untapped does the same. It finances productive assets and gets paid back with the revenues these assets generate.

What type of assets does Untapped finance? Cars? Motorbikes? Generators? Well, all of them. It doesn’t really matter.

And here is what distinguishes Untapped from Moove, and what makes their model more interesting and more scalable.

2) Operating partners ⛑️⛑️⛑️

Moove is good at financing cars for Uber drivers. It is not a trivial task and they had to become good at it.

Why? Two reasons.

First ☝🏽, managing a fleet of vehicles demands domain expertise and operational overhead.

Moove needs to develop proprietary tech & manage the integration with Uber to have visibility on how the vehicles are utilized, how much revenue is generated, and receive timely payments. It is a lot of plumbing.

They also need to partner with car manufacturers for steady supply & support services, and create a system to onboard drivers and evaluate their creditworthiness and performance. Again, a lot of plumbing.

Second ✌🏽, Moove itself is subject to credit risk. They don’t purchase the vehicles from their balance sheet money: it would be too capital-intensive. They have to take up loans/financing from creditors. And given they offer revenue-share deals to their drivers, they have to juggle between variable repayments from drivers vs fixed installments they owe their creditors.

This is the main reason we don’t see many companies like Moove around. While revenue-share agreements are attractive to drivers, part of their business risk rolls up to the company borrowing them.

Now, how does Untapped fit in this picture?

“We don’t know how to manage a fleet of vehicles”, says Lundie.

“We partner with the likes of Moove, who know the realities on the ground, and relieve them from part of their credit risk by striking a revenue-share agreement with them”.

“We don’t want to replace Moove. We want to invest in dozens of the best Mooves across multiple industries, geographies, currencies - and be their complementary source of capital”.

In this sense, an operating partner is a company focused on one vertical (like Moove with cars).

No matter if, instead of cars, the company is financing electric bikes, solar-powered irrigation equipment, smart refrigerators, or thermal printers. As long as it:

knows how to manage operations on the ground, and

has the technical skills to collect & integrate data from the assets and the underlying businesses

Untapped can invest in it!

As a result, the interests of all the actors, from the drivers to the Mooves, to the ultimate investors in the physical assets, are aligned. Aligned along what? Well, the revenues the assets generate!

A little sketch:

Ok cool, so how does Untapped manage its own risk?

3) Iterative approach 🌀🌀🌀

“We always invest in two stages. No matter the size of the company, at the beginning every operating partner starts with a pilot”.

This means $50-100k as a first check for a 4 to 6-month period: “We put money in your hands and see what you can do”.

In practice, this helps the team tick some boxes: how many assets can you deploy? What is the quality of your data? Can you integrate data with our platform? Can you pay back in time?

If the results are good, the company enters a scaleup stage, where investments range from 500k to 5M.

At this stage, the operating partner is expected to have already managed the data integration and be working on the payment integration, which is the hardest part (moving money from local wallets in Ghana to local wallets in the US, for example).

Out of 59 companies, only 7 have entered the scaleup phase.

“Our goal is to really pick up the best ones, those who need 5 million a year, and can achieve that scale and the impact”.

This approach of spreading the seeds and harvesting the good ones allows Untapped to manage risk efficiently while gathering loads of data.

And it’s ultimately in the data that lies the core competitive advantage of this model.

4) Real-time data 📈📈📈

Imagine a world where, when you invest in an African entrepreneur, you can have visibility on where each asset is deployed and how much money it’s making, in real-time. This is the vision of the Smart Asset Financing platform developed by Untapped.

How hard is it to integrate data from assets and businesses across different regions?

“This is our real edge. We want to be tech-driven, so our data team is working to do what currently no one is doing”.

What no one is doing is the following:

integrate data from physical assets

with data from underlying businesses using these assets (i.e. revenues),

from multiple operating partners who deployed them (i.e. tens of Moove, across business verticals);

To do what?

Monitor your entire portfolio in real time,

paying your investors as the money comes in,

develop proprietary risk management models

To me it sounds a bit like a command center, where you can say: “OK, we financed 10,000 entrepreneurs. What is happening on the ground? How well the money is moving around? How much are we making? Should we scale-back on something?”

It’s a pretty compelling vision.

The question then is, how far are we from a world like this?

“Data integration and especially payment integration, is still hard. We need to provide technical assistance to some of our earlier stage operating partners because not everyone has those capabilities yet”. Also, “moving money from local wallets to regional wallets to the US, is still a headache, and a problem that no one completely solved yet”.

Smart Asset Financing is the first iteration aiming to deliver on this promise, and challenges of this kind can only be solved with tunnel vision.

So what’s in it for us? 🤷🏽🤷🏽🤷🏽

After the conversation I had with Lundie, my brain was like “There needs to be more of this”. If we take it back from where we started, it’s a no-brainer.

SMEs are the lifeblood of the African economy.

To continue delivering products and services each of us needs, they need capital to purchase and maintain physical assets.

IoT, digital payments and the smart distribution of risk & operational overhead, have paved the way in solving the two major bottlenecks preventing traditional banks from helping them: credit risk modeling and data availability.

Untapped has worked its way through novel ways of addressing this challenge. Others are doing that too. We need to learn from them, copy and iterate.

How much more wealth would there be if there wasn’t just one Moove, but one hundred Mooves?

How much more resilient our economies would be, if, instead of just cars, we could finance irrigation systems, trucks and medical devices?

I don’t know, but I definitely want to hear more stories like this.

smart article!

"the value of collateral assets can be required to be up to 80-100% of the value of the loan" more like 150% of the loan!